Investment Research Note – January 9, 2019

Review:

After one of the worst Decembers in history, investors should be happy to flip the calendar to 2019. The year of 2018 will go down as the toughest market environment since the Financial Crisis of 2008-09. After a strong 3rd Quarter where we saw major US stock indices hit fresh all-time highs, the 4th quarter was characterized by relentless selling and non-stop negative news.

For the 4th quarter, the S&P 500 was down -13.52% on a total return basis, the worst quarter for large US companies since the 4th quarter of 2008. In December alone, the S&P 500 was down -9.03%, the worst month since February of 2009 and the 11th worst month for the S&P 500 going all the way back to 1928. On a total return basis, the S&P 500 was negative for the first calendar year since 2008. That streak of nine straight positive years has tied for the longest in history.1

While many point to the interest rate increasing efforts of the Federal Reserve as the primary catalyst of market weakness, we believe it was actually a collection of factors that conspired to turn the tide including but not limited to: the elongation and exacberation of trade war with China, the government shutdown and general dysfunction in DC, a slowing trend in Chinese economic reports, softening US Housing data and an uncertain outlook from US corporations should all be considered in the mosaic of negativity that underwrote the “risk-off” environment.

What really added insult to injury for investors last year was the lack of any redeeming asset classes, styles, geographies, sectors, or strategies that offered positive returns, aside from cash.

While 2017 was a year in which asset categories were nearly all green, 2018 was a year in which asset categories were nearly all red. From this angle, it’s nice to move on from last year to reset investor pyschology.

Equities:

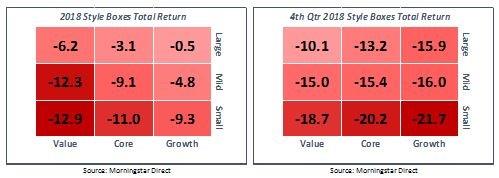

While US Large Cap stocks struggled, US Small Cap and US Mid Cap stocks did worse….they were down -20.2% and -15.4%, respectively, for the quarter. It was a trapeze-like year of highs and lows for US Small Caps – at one point in June, the Russell 2000 Index was outpacing the S&P 500 by over 7% before giving all of that up and more during the 4th quarter.2

US Growth stocks outperformed Value stocks for the third time in four years, although the margin narrowed in the 4th quarter.3

Healthcare, Consumer Discretionary and Utilities were the best performing, and only positive returning, S&P 500 sectors last year. During the 4th quarter, only the Utilities sector was positive. As commodity prices fell sharply, Energy and Materials were the laggards. Financials (a Wall Street favorite going into the year) were also notably weak on falling rates and concerns about loan credit quality. That sector fell -17.3% during the 4th quarter.4

Internationally, both Emerging and Developed Markets struggled throughout the year as well. The MSCI Emerging Market Index ended the year down -14.6% while the MSCI EAFE (Europe, Asia, Far East) Index was down -13.8%. After underperforming the US for the first three quarters of the year, international stocks actually were relative outperformers during the December sell off.5

Fixed Income:

For the first 11 months of the year it appeared that bonds, as measured by the Bloomberg Barclays US Aggregate Index, would decline in value for the first calendar year since 2013. However, due to the massive flight to quality and drop in Treasury rates during December, bonds rebounded to finish positive, +0.01%, for 2018.6

December was the best monthly performance for the broad fixed income index since December 2008. This performance goes to show how high-quality bonds remain the “old faithful” of diversification in times of equity market disruption.7

The 4th quarter’s “risk-off” environment caused flows out of corporate credit instruments, with Bank Loans and High Yield bonds losing -3.1% and -5.4%, respectively, during the quarter. Higher quality fixed income, like US Treasury and Agency securities as well as Municipal bonds fared the best due to positive returns during the sell-off as investors sought safety.8

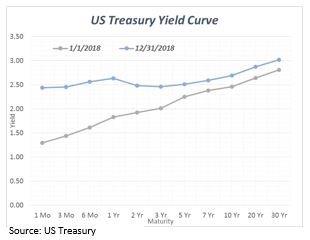

The potential inversion of the yield curve, as shown below, was a hot topic all year and will continue to be during 2019. As of 12/31/18, the 1-year Treasury was yielding more than the 2-, 3-, 5- and 7-year maturities which is technically an inversion. There is a closer eye on the 10-year minus 2-year spread and the 30-year minus 2-year spread, both of which have yet to invert. The short end has continued to rise as the Fed tightens their target rate while intermediate and long rates plummeted during the last six weeks of 2018.9

The benchmark 10-year Treasury made big moves during 2018. It began the year yielding 2.46% and rose to a high of 3.24% on November 8th. And once the equity market sell-off intensified, investors rotated to Treasuries and yields dropped back to 2.87% by the end of the year.10

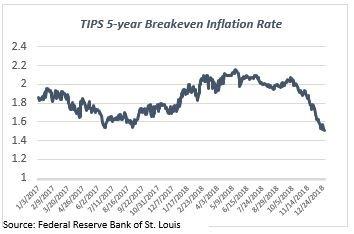

It appears that another root cause of the drop in yields was a significant pull back in inflation expectations. As shown in the chart to the right, the breakeven rate, (a market based indicator for expected inflation), for 5-year Treasury Inflation Protected Securities (TIPS), peaked in May 2018 at 2.2% before dropping off of a cliff to 1.5% at the end of the year.11

Nowhere to Hide:

It can be perceived that the resonating theme of 2018 is how almost nothing “worked” for the investor. Certain areas of the market had intermittent periods of gains, but from point to point the year was difficult across the board. Cash, and after a strong showing in December – high quality bonds, were the only exceptions.

There were essentially no areas of the market insulated from the pain. Morningstar provides data on 105 mutual fund categories. Of those 105, only 21 were positive for 2018. Of those 21 positive categories, 15 were Municipal bond categories, 4 are high quality/government or Ultrashort bond categories and the other two are the Utilities and Bear Market (short-biased fund) categories.12

In most cases, every other category spanning the investment landscape was negative – whether it’s a style, sector, or geographic specific Equity category, an Alternative like Long/Short Equity or Managed Futures, or a Real Asset category13. For the diversified investor this added to the frustration – as core US equity exposure was weak so was pretty much everything else. The table below from Morgan Stanley, demonstrates this phenomenon well and how rare it is14:

Bear Market? :

Much has been made about the ongoing Bull market rising out of the Financial Crisis being one of the longest in history. It’s a debate that shouldn’t matter very much. The standard definition of a Bear market is a 20% drop from the peak based on closing prices. So technically, the S&P 500 has not become a Bear market since it only fell -19.78% during the most recent drawdown closing on Christmas Eve 2018 (it fell past -20% on December 26th before rallying). Also, technically it didn’t reach one in 2011, although the decline exceeded 20% on an intraday basis too, the market never closed below the threshold. So whether or not this is an official Bear or just a “Correction” we believe is a silly argument. There’s no reason why -20% is any more painful than the 22 basis points between the -20% line and -19.78%.15

There’s also no great reason why just because the most closely followed US Large Cap Index (S&P 500) doesn’t fall 20% that the market doesn’t have the feel of a true Bear. Consider some major broad areas of the market that did fall 20% plus during the turbulence: NASDAQ Composite (-23.4% drawdown), Russell 2000 (-26.9%), EURO STOXX 50 (-24.1%), MSCI EAFE (-20.9%), MSCI Emerging Markets (-25.0%). And then those more specific areas of the market that saw even worse: WTI Crude Oil (-43.9%) and the Energy sector (-30.4%), Germany’s home country DAX Index (-29.0%) and China’s (-31.1%).16 And perhaps the best sign of a bear market is looking under the hood of the major index to find that exactly 60% of stocks in the S&P 500 were in a bear market (20% below their highs) on December 19th.17

Corrections and Bear Markets are typically a characteristic of Equity investing as a risk asset. The current drawdown is actually no different than any other during the market cycle – even though it always seems to be more painful when you’re in the eye of the storm. This current decline is the 23rd drop of 5% or more since March of 2009, it’s the 7th drop of 10% or more and the 2nd drop of 20% or more during that time.18 Since 1945, declines between 5-10% tend to happen annually, declines of 10-20% happen about every 3 years and declines of over 20% happen about every 5 years.19

Outlook:

So far in 2019, we’ve seen a couple positive developments for the market. Fed Chair Powell’s comments on Friday (1/4/2019 acknowledged the market distress and was open to adjusting the Fed’s Balance Sheet if need be.

Second, there are mid-level trade talks scheduled to take place this week (1/7/2019-1/11/2019) between the US and China that could show signs of progress towards a resolution – both countries should be incentivized to make a deal just by the material effects of the trade war now showing up in market and economic data.

The economic and corporate profit outlook remains positive. Earnings are forecasted to grow at 7.4% for 2019 for the S&P 500, while the top line revenue is forecasted to grow 6%.20 Well off the meteoric rises of 2018 but nonetheless still growing over a high hurdle. Earnings season, which kicks off soon will have to be monitored closely.

As prices have fallen, so have valuations for the market – which is typically more advantageous entry point for investors. In fact, during 2018 the market saw the largest multiple compression since back in 2002 as the trailing P/E ratio fell by over 25%.21 At this point, the forward and trailing P/E ratios sit below their recent historical averages for the S&P 500.22

While the US economy will likely not see the acceleration it saw in 2018 but the outlook still calls for positive real GDP growth. The latest projections from the Federal Reserve call for a range of 1.7% to 2.4% real GDP growth in 2019.23 While fears of a recession flared up driven by softness in Housing and Autos, a potential inversion of the yield curve, tighter credit, the recent stock market drop and some disappointing Purchasing Manager’s Index data, most indications are that a US recession in 2019 would be an unlikely event given the impressive strength in the job market. Consumption continues to make up the bulk of GDP (68% in the 3rd quarter 2018)24 and buoyed by the recent tax cut, spending is strong and consumer balance sheets are sound.

– John Nagle, CFA

The views expressed herein are those of John Nagle on January 9th, 2019 and are subject to change at any time based on market or other conditions, as are statements of financial market trends, which are based on current market conditions. This information is provided as a service to clients and friends of Kavar Capital Partners, LLC solely for their own use and information. The information provided is for general informational purposes only and should not be considered an individualized recommendation of any particular security, strategy or investment product, and should not be construed as, investment, legal or tax advice. Past performance does not ensure future results. Kavar Capital Partners, LLC makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based on information that Kavar Capital Partners, LLC considers reliable, it is not guaranteed as to accuracy or completeness. This information may become outdated and we are not obligated to update any information or opinions contained herein. Articles may not necessarily reflect the investment position or the strategies of our firm.

This market commentary is a publication of Kavar Capital Partners, LLC. It should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the author on the date of publication and are subject to change. Content should not be viewed as personalized investment advice or as an offer to buy or sell, or a solicitation of any offer to buy or sell the securities mentioned herein. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be suitable or profitable for a client’s investment portfolio. All investment strategies have the potential for profit or loss. Asset allocation and diversification do not ensure or guarantee better performance and cannot eliminate the risk of investment losses. Asset allocation and diversification do not ensure or guarantee better performance and cannot eliminate the risk of investment losses. Charts and graphs do not represent the performance of Kavar Capital Partners, LLC or any of its advisory clients. Historical performance results for investment indexes and/or categories, generally do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment management fee, the incurrence of which would have the effect of decreasing historical performance results. There can be no assurances that a client’s portfolio will match or outperform any particular benchmark. Projections and opinions are based on assumptions that may not come to pass. Data is derived from sources deemed to be reliable. Kavar Capital Partners, LLC is registered as an investment adviser and only transacts business in states where it is properly registered, or is excluded or exempted from registration requirements. Registration as an investment adviser does not constitute an endorsement of the firm by securities regulators nor does it indicate that the adviser has attained a particular level of skill or ability.

Footnotes:

- Morningstar Direct Data

- Morningstar Direct Data

- Morningstar Direct Data

- Morningstar Direct Data

- Morningstar Direct Data

- Morningstar Direct Data

- Morningstar Direct Data

- Morningstar Direct Data

- US Treasury (https://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=yieldYear&year=2018)

- US Treasury (https://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=yieldYear&year=2018)

- Federal Reserve Bank of St. Louis (https://fred.stlouisfed.org/series/T5YIE)

- Morningstar Direct Data

- Morningstar Direct Data

- Morgan Stanley (https://www.morganstanleyfa.com/public/projectfiles/onthemarkets.pdf)

- Morningstar Direct Data

- Morningstar Direct Data

- CNBC (https://www.cnbc.com/2018/12/19/most-of-the-sp-500-is-already-in-a-bear-market.html)

- Pension Partners/Charlie Bilello (https://pensionpartners.com/2018-the-year-in-charts/)

- AAII: The American Association of Individual Investors (https://www.aaii.com/journal/article/stock-market-retreats-and-recoveries)

- FactSet Earnings Insight (https://www.factset.com/hubfs/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_010419.pdf)

- Pension Partners/Charlie Bilello (https://pensionpartners.com/2018-the-year-in-charts/)

- FactSet Earnings Insight (https://www.factset.com/hubfs/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_010419.pdf)

- Federal Reserve Economic Projections as of 12/19/2018 (https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20181219.pdf)

- JPMorgan Guide to the Markets (https://am.jpmorgan.com/blob-gim/1383407651970/83456/MI-GTM_1Q19_.pdf?segment=AMERICAS_US_ADV&locale=en_US)