When Push Comes to Shove

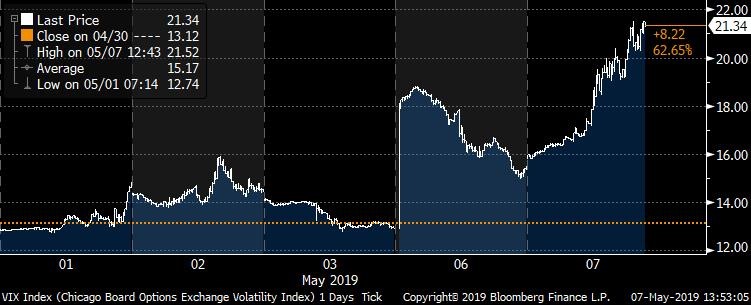

In just the last week or 2, financial markets have exhibited a trait otherwise absent thus far in 2019: volatility.

Courtesy of a combination of trade-talk consternation and earnings ambiguity, large intra-day price swings, heavy put option/protection buying and a bounce in the VIX (see below) have all emerged.

Volatility is typically associated with “fear,” and “fear” is one acclaimed catalyst of elevated trading activity. The other, commonly, is “greed”.

The market’s emotional pendulum swings between these 2 characterizing conditions – prompting paranoia or partying.

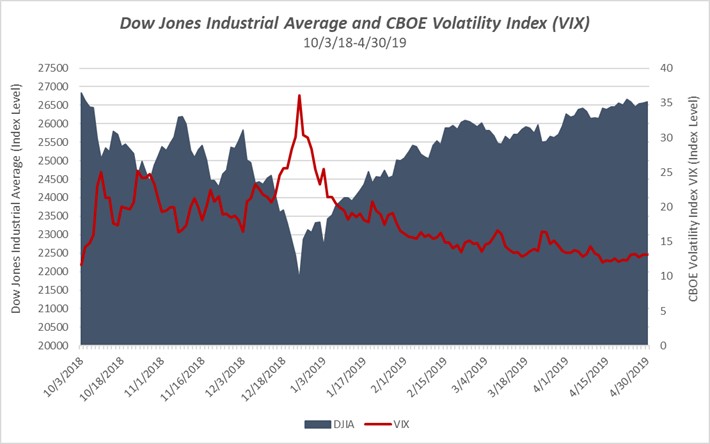

When the markets are in a downtrend and fear trumps greed, volatility spikes. The 4th quarter of last year is a great near-term reference point.

When markets are in an uptrend and greed trumps fear, volatility goes dormant. The first quarter of this year is a great nearer-term reference point.

While there is an old expression on Wall Street that the market tends to go up like an escalator and down like an elevator, the last 6 months have shattered that imagery…..think bungee cord!

Source: Morningstar Direct

Such a snap-back has served as a salve for some.

Healing has come quickly as all-time high levels of the most-watched indices have been eclipsed and volatility has been hibernating, or at least on hiatus.

However, this month has ushered in an awakening.

Anyone who was has invested money for a little while or even just casually watches the market knows this: dormancy is delicate as it relates to volatility and complacency is concerning as it relates to investor attitudes.

And while the presence of volatility can be broadly unsettling, it does offer opportunities that are otherwise evasive.

To that end, I cannot help but be reminded of a great song from the popular musical, Hamilton: “You’ll be Back” https://www.youtube.com/watch?v=Rgiyq7rqWhg

Sung by the spurned King George III of England, its essence is a warning to a likely-to-be-liberated New America on the expectations of existing in the absence of royal rule.

The operative lines are as follows:

“You’ll be back, soon you’ll see; you’ll remember you belong to me……

You’ll be back, time will tell, you’ll remember that I served you well….”

While the king warns that taking ownership of one’s destiny may be noble, doing so with the expectations of only smooth sailing is a misnomer.

In much the same fashion, though less snappily stated: wanting to emancipate markets from volatility would be a structural impediment to long-term investing success. Here are 3 reasons why:

1. Valuation check-points. As stated famously by Warren Buffett: “When the tide goes out, you can tell who is skinny-dipping.”

When financial markets are quiet, have healthy tail-winds, and are underwritten by optimism, it may be easier to overlook things about a company/country/asset class that deserve deeper inspection.

Nothing sharpens the focus like a risk of loss. The scrutiny meter against which economic judgments are made calibrates more keenly in the presence of volatility as taking anything for granted seems ill-advised.

It is in this mode that “benefits of the doubt” give way to “proving points”. And as this takes place collectively across markets, valuations emphasize evidence as opposed to aspirations. That is healthy.

2. Reacquaintance w/ risk. Almost all investor risk-profiles consider the following inputs when assembling an appropriate portfolio: time horizon, need for income and, let’s call it: intestinal fortitude.

This final input is the only qualitative one and therefore, non-linear. To be fully aware of your threshold for portfolio variability, it is most helpful to have encountered it in the past.

It is at the intersection anecdotal and empirical where true long-term asset allocation comfort resides.

Having periodic reminders of why the pie charts on your monthly account statements are colored as they are is beneficial – economically and, more importantly, emotionally.

3. Opening of entry points. It has been said that an investor can be price-sensitive or outlook-sensitive, but not both.

When investing in publicly-traded common stocks (or mutual fund/ETF conduits), we are mostly outside, passive, minority investors. Therefore, a disciplined adherence to price sensitivity is critical to effectively deploying capital.

Were volatility non-existent and were prices to only go up, a disciplined investor would possess few opportunities to find attractive entry points and be biased to more defensive classes of assets – impeding the attainment of long-term performance objectives.

In addition, the principal of dollar-cost-averaging (most often enacted in retirement savings plans) revolves around the methodical funding of asset classes according to a designated percentage target (for instance, 30% large company stocks, 10% international stocks, etc.)

These percentage targets are being fed from a fixed amount of capital (payroll deduction) and the higher the price of any asset in the allocation, the fewer the number of purchased units. Conversely, the lower the price, the higher number of units.

The smoothing effect that transpires over time as investors track toward their retirement goals is an embedded benefit of, yep, volatility.

So while we are seeing the first teeth of 2019’s volatility, it does not need to be biting. Ultimately its presence is positive. It is cleansing and it is cathartic. And in the aforementioned words of King George III, it will serve us well.

Important Disclosures:

The views expressed herein are those of Douglas Ciocca on May 7, 2019 and are subject to change at any time based on market or other conditions, as are statements of financial market trends, which are based on current market conditions. This information is provided as a service to clients and friends of Kavar Capital Partners, LLC solely for their own use and information. The information provided is for general informational purposes only and should not be considered an individualized recommendation of any particular security, strategy or investment product, and should not be construed as, investment, legal or tax advice. Past performance does not ensure future results. Kavar Capital Partners, LLC makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based on information that Kavar Capital Partners, LLC considers reliable, it is not guaranteed as to accuracy or completeness. This information may become outdated and we are not obligated to update any information or opinions contained herein. Articles may not necessarily reflect the investment position or the strategies of our firm.