Market Update – December 17, 2018

The financial markets picked up today where they left off on Friday. More appropriately stated, they picked down.

Given its propensity for positive performance, December is known as a seasonally strong month for markets. Such has not been the case thus far this year.

Only 11 trading days into the month and the S&P 500 is tracking a decline rivaling that last seen in 1931.

Yes, 1931. Quick points of reference: in 1931, the unemployment rate averaged 14.2%1 for the year, real GDP shrank by 6.41%2 and there was not only no inflation…..there was a 7.02%2 rate of deflation for that year!*

Not to suggest that markets trade directionally pure with the economies within which they exist, but they do to tend to offer insights as to their fiscal fortitude, if not always the prevailing sentiment.

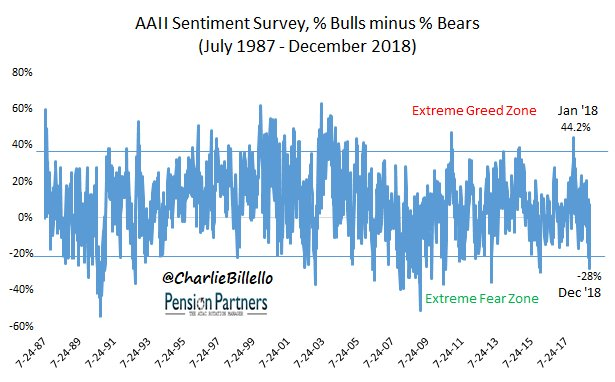

Speaking of sentiment, to put it mildly, it stinks.

As the chart below depicts, Bearishness is boiling…..so much so that it may be Bullish.

When Bearish sentiment reaches levels of extreme fear, which it did today, it has portended well for both short and long-term return potential:

Source: Charlie Billello/Pension Partners

And the only thing that seems to repeat more reliably than history is human behavior. This of course was the inspiration behind Warren Buffett’s famous advice to, “Be fearful when others are greedy and greedy when others are fearful.”

I am not suggesting that the market will turn around immediately or that volatility is due to dissipate, but it seems likely that the sentiment swing has been excessive, offering some interesting opportunities and entry points.

It is difficult to envision the rest of trading this week being much less frenetic than it was today – which does not imply a negative bias.

This week is loaded with news flow and data points including: BREXIT hearings, economic speeches by the President of China and the President of Japan, a Federal Reserve Bank meeting and the deadline for a US Government shut-down. Chock-full.

Given the burden borne by the head of the Fed, Jay Powell, for triggering the bulk of this Fall’s market madness, (https://www.cnbc.com/2018/10/03/powell-says-were-a-long-way-from-neutral-on-interest-rates.html), I think that his actions and comments @ the conclusion of Wednesday’s meeting will be critical to the footing on which the markets conclude the year.

The consensus is that the Fed will raise interest rates on Wednesday. According to Bloomberg: 88 of 90 economists surveyed estimate an increase.

Much has been written about the Fed “needing” to hike to defend their credibility.

Chairman Powell’s most vocal critic, President Trump, has been incessantly insistent that the Fed is overtightening interest rates, even before any moves made this week. Many speculate that Powell will raise rates solely to emphasize his immunity from influence. I am hopeful that does not enter the calculus.

Perhaps Powell’s most qualified critics co-authored an Op/Ed in the weekend Wall Street Journal. Penned by a former Fed Governor, Kevin Warsh, and a legendary investor, Stan Druckenmiller: https://www.bloomberg.com/news/articles/2018-12-17/druckenmiller-urges-fed-to-pause-tightening-blitz-in-wsj-op-ed, the pair contend that the Fed has gone far enough.

“We believe the U.S. economy can sustain strong performance next year, but it can ill afford a major policy error, either from the Fed or the rest of the administration,”

I think that they are generally correct but also adhere to the adage, “it’s not what you do, it’s how you do it.” Should the Fed raise rates on Wednesday, how they set expectations for the future will be even more important.

Raising rates is, “in the market” and the act itself offers no new information. Setting the stage for the future is where the rubber meets the road. And keeping this economy on the track is certainly in the Fed’s best interest.

They certainly understand that the preservation, availability and affordability of liquidity is vital to restoring confidence in capital markets. And confidence, right now, is sorely lacking.

We’ll be in touch later this week as more of the information mentioned above unfolds.

1 Source: National Bureau of Economic Research

2 Source: U.S. Bureau of Economic Analysis

* Today’s data: 3.7% Unemployment rate, +4.2% GDP Growth in Q2’18 & projection of +3.5% Q3’18, CPI = 2.2% Y/Y – all sourced from Bloomberg Market Data

The views expressed herein are those of Doug Ciocca on December 17, 2018 and are subject to change at any time based on market or other conditions, as are statements of financial market trends, which are based on current market conditions. This information is provided as a service to clients and friends of Kavar Capital Partners, LLC solely for their own use and information. The information provided is for general informational purposes only and should not be considered an individualized recommendation of any particular security, strategy or investment product, and should not be construed as, investment, legal or tax advice. Past performance does not ensure future results. Kavar Capital Partners, LLC makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based on information that Kavar Capital Partners, LLC considers reliable, it is not guaranteed as to accuracy or completeness. This information may become outdated and we are not obligated to update any information or opinions contained herein. Articles may not necessarily reflect the investment position or the strategies of our firm.